Build It And They Will Come, Educate Yourself, What's My Rate Again?

Tuesday Tips for Realtors: 04/22/2025

Watch The Highlights Here:

Top Story:

Build It and They Will Come

Another major company expanding in Texas?

It may be hard to hear the good news in the real estate community, but it's out there if you look in the right places. With all the concerns of prices and tariffs, there is news making its way around America—and honestly, it’s about time.

With companies like Nvidia announcing plans for massive new chip factories right here in Texas (yep, both Houston and Dallas are getting in on the action), it feels like we may be rounding the corner for a potential turning point for U.S. manufacturing and the communities that depend on it.

There is a school of thought that if you live in an area that stops building and developing, you need to start to worry. Growth and constant construction may be a headache for traffic, but those same annoyances mean jobs, career growth, and improved real estate values and demand. This type of growth lays the groundwork for entire ecosystems to thrive for years to come. Nvidia’s move is a perfect example. They’re not only bringing high-tech manufacturing stateside, but they’re also partnering with giants like Foxconn and Wistron (manufacturers for Apple) to make it happen. We’re talking about over a million square feet of new production space, with mass production set to start in just over a year. I, for one, cannot wait!

Switching gear to residential real estate:

Real estate has been on a wild ride for years now, and we all know it. High interest rates, tight inventory, and aging homes have made it tough for buyers—and let’s be honest, not every “charming fixer-upper” is worth the headache. But that does not mean there isn’t an opportunity out there.

That’s where the build-to-rent (BTR) trend comes in. More and more investors seem to be shifting their focus to this strategy, new rental communities, especially in places like Dallas-Fort Worth, which now leads the nation in new BTR construction.

Why not just buy existing builds? Simple: Inventory for the price of homes does not get you the quality you would expect at the price points they are currently holding at. Also, there are still plenty of bidding wars happening at certain price ranges. Build-to-rent offers modern layouts, energy efficiency, and the kind of amenities today’s renters expect. For investors, it’s a win-win: steady income now, fewer overall maintenance and updates, and the potential for big equity gains down the road as these communities appreciate in value.

The numbers support the strategy. Last year, Texas started nearly 22,000 new BTR homes, with DFW leading the charge. And it’s not just young professionals or families driving demand—remote workers, empty nesters, and even downsizers are all looking for that sweet spot between flexibility and comfort.

Building costs are rising, and we have no idea where they are heading. This factor alone will impact maintaining the market’s demand for Instagram quality. This is where building a reputation is a must. Several people watch HGTV, and they can be flippers overnight. Sadly, the same happens in new builds. It’s the wild west here in Texas when it comes to construction regulation, and cutting corners is not going to be the solution to circumvent building costs. The only way to save on costs is to double down on smart building design, sustainable materials, and effective property management, allowing the build to last for years, rather than requiring new updates after just one tenant. That’s how you continue to attract tenants who stick around and investors who see real returns.

So, what’s the takeaway? The momentum we’re starting to see—from Nvidia’s factories to the surge in build-to-rent communities—proves that if you invest in quality and meet people where they are, the demand will follow.

We’re at the start of something big. And as someone who’s passionate about seeing our cities and neighborhoods grow, I can’t help but feel excited for what’s ahead. Build it, and they really will come.

I leave you with two quotes that have really hit home for me lately, so much I included them in my weekly Mortgage Webinar for Clients.

“Buy land, they aren’t making any more of it.” - Mark Twain

“I will forever believe that buying a home is a great investment. Why? Because you can’t live in a stock certificate. You can’t live in a mutual fund.” - Oprah Winfrey

References:

NBC DFW - Rental Home Construction

EliseAI.com - Rental Home Construction

CBS News - Nvidia Plans

Top Growth Tip:

Educate Yourself

Last week, when I dropped the great information of Mike Simonsen at Altos Research (free, crazy awesome area reports!), I was shocked by how many agents of the next few days told me they had never heard of him or Logan Motashami. These two guys are the smartest people out there when it comes to market data and mortgage rate movement. You need to make these two a part of your weekly news feed.

With that in mind, I thought I'd share some other important real estate-related news sources for this week. There is a good chance you don’t know all of these, so check them out, make them a part of your regular workweek, and level up your game as the Real Estate Pro your clients know you to be.

It sounds boring, but you have no idea how much easier it is to talk this stuff when you have even just a few moments each week to absorb it.

Top Real Estate News Publications:

HousingWire ← , It shocked me this week how many agents never heard of this publication!

Top Lending Tip:

What’s My Rate Again?

I am going to get on my soapbox here. Sorry, not sorry.

Meeting realtors, they seem to have a natural defense, almost like someone in a committed relationship. “I already have dedicated lender partners.” Which I can 1000% respect, our entire business is built on networking. So, keep your dedicated partners, but I ask that you make sure they are really your “partners”. If they aren’t making you better, are they really your partner?

“What’s your rate?” - I am sure everyone reading this has asked that sometime recently, maybe even today. That question is expected from prospective clients, but it always surprises me when I hear it from an agent.

Any agent with a dedicated lending partner should have a clear understanding of how mortgage rates work. They may not be able to teach a class, but they certainly should understand how loaded that question is. This question is so important to understand that I have a whole section dedicated to it in my Mortgage Essentials for Realtors Webinar on Thursdays.

Let’s start with the basics:

The 10-year bond influences mortgage rates. Several factors can impact shifts in rates, but ideally, mortgage rates move in line with the 10-year bond.

There are main categories that impact mortgage rates:

Product: FHA, VA, Conventional, USDA, Hard Money, Non-QM

Occupancy Type: Owner Occupied, Investment, Second Home

Term: 30 years is much different than a 15-year mortgage.

Loan-to-Value: Less money down = higher risk of loss in default

Credit Score: Considered in score ranges. Your consumer report card, how you pay others, reflects how you could pay this mortgage.

There are other adjustments to the mortgage, called Loan Level Pricing Adjustments. These are typically related to Fannie Mae and Freddie Mac, but all lenders have them to some extent. That's why rate sheets look like something out of The Matrix - numbers everywhere. It’s hard to easily decipher which rate applies to which scenario. (Thank goodness for rate engines!)

Here are just a few examples of loan-level pricing adjustments that lenders can implement.

Credit History: late pays, defaults, credit events, thin credit

Occupancy: Non-Occupancy Co-Borrower

Employment History

Location of Property

Property Type

Loan Amount

Debt-to-Income

Borrower Classification

Note: At any time, the lender can choose to apply a rate adjustment for any “exception” they deem necessary to help offset the loan's risk. Basically, make more on the loan while they can in case of a default.

To wrap this up, prepare borrowers and yourself to dive into client scenarios when discussing rates. I have rates in the 4s up to the 9s, but there is no way to tell which rate is the best scenario for the client. I could quote a 5.75% rate, complete the application, and then find out that it makes more financial sense for the client to go with a 6.5% rate based on closing costs, reserves, and their financial goals for the next few years. Or it could be beneficial to go the opposite way, from high to low, based on those same factors. Rates come with costs, whether it's an origination fee, a discount fee, or built into the rates (yes - it’s a thing).

Give me a call and we can talk all about rates!

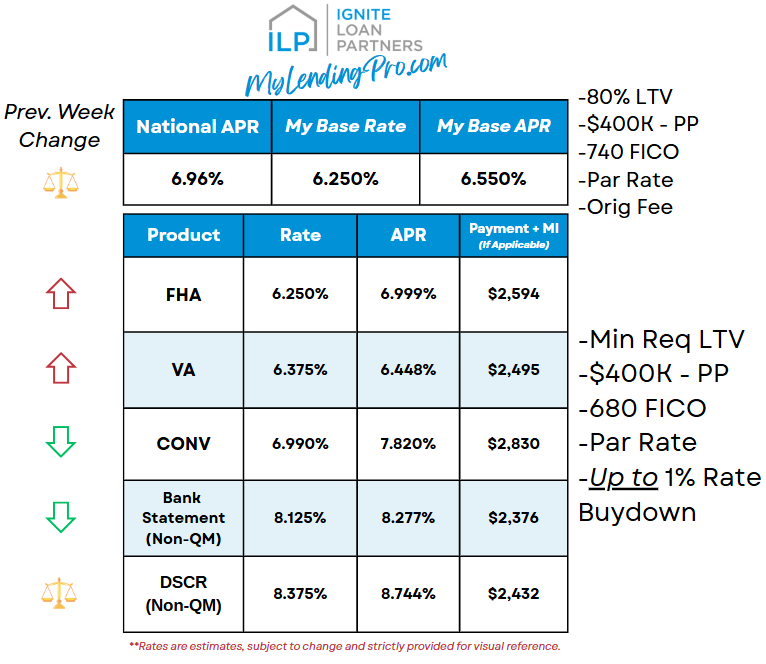

Quick Rate Reference guide for 4/22/2025: ⚖️

The following rates are for visuals to help you see where rates are. These are never final and are intended to be a more realistic look than what you find advertised on popular sites. All rates are subject to client scenarios and are subject to change. Thank you for using common sense when reviewing! 😊

Overview:

Rates overall haven’t moved much.

Government loans have seen a slight pricing increase.

Bank statement loans for self-employed clients are the winners this week, as pricing and par rates have dropped.

Overall, not much has changed, depending on how the headlines continue to develop closer to the next Fed Meeting on May 6- 7th, and if there is any truth to firing Powell, which would be horrible per Logan (and I agree)!

Mortgage rates follow the bond markets, but all markets react to each other, and they seem to react to what the Fed does!

I thank you all for reading, and I hope you are having a great start to your spring season! If you need ANYTHING, just reach out and ask. I have your back if you need someone to cover it!